· Federal Contracting · 8 min read

Bonding Requirements for Federal Construction Contracts: What You Need to Know

Most federal construction contracts over $150,000 require a performance bond and a payment bond before you can even be awarded the work. Here is what bonding is, how to get it, and what to do if you cannot qualify yet.

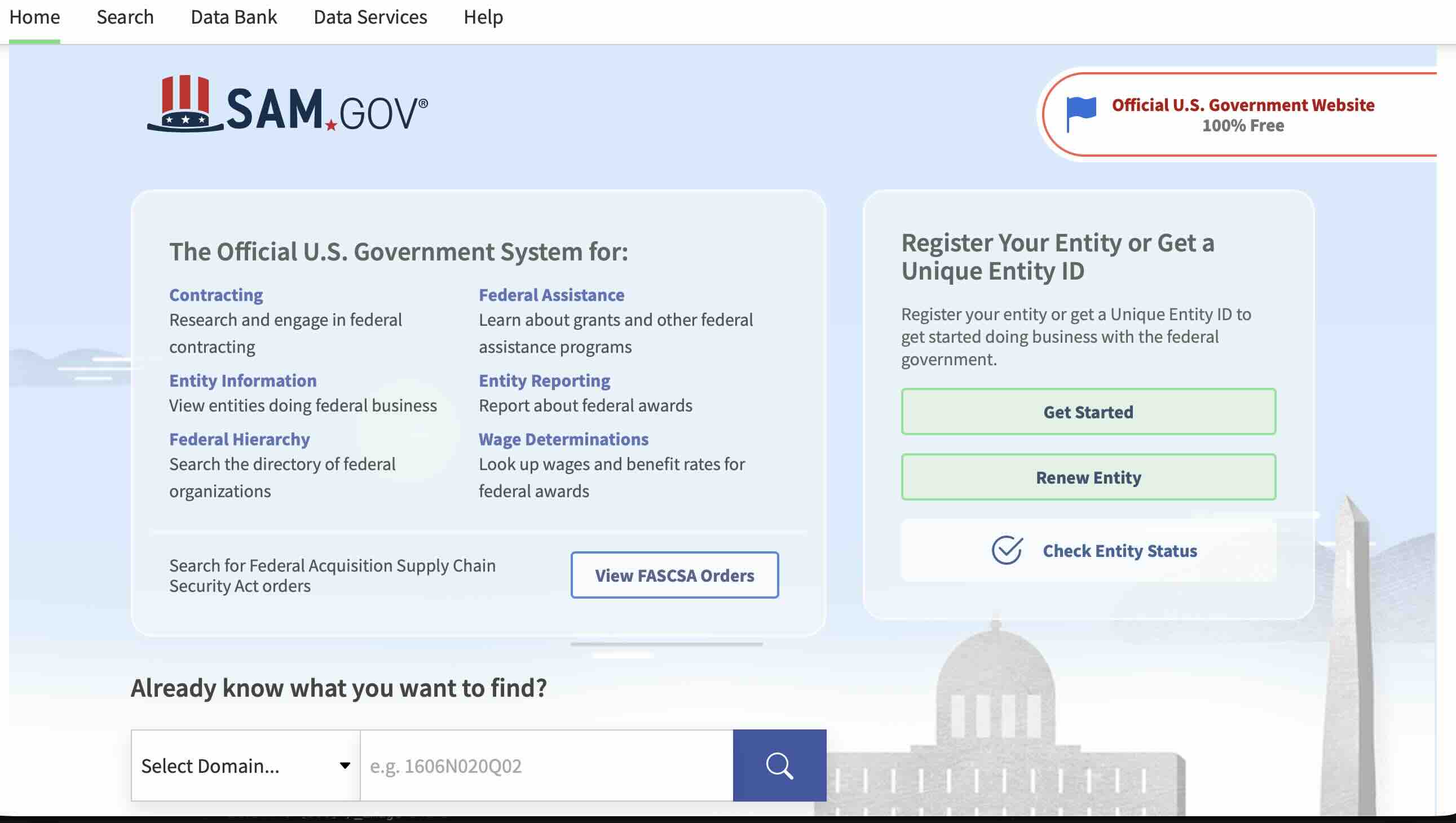

If you’re looking at federal construction jobs on SAM.gov, bonding is the first thing that will stop you in your tracks. Not paperwork. Not competition. Bonding. A lot of smaller contractors get excited about a government opportunity, spend time reviewing the solicitation, and then find out they can’t bid because they’re not bonded or their bond capacity isn’t high enough for the contract value.

This post covers what bonding actually is, when it’s required, what it costs, how to qualify, and what to do if you can’t get bonded on your own yet.

Why the Federal Government Requires Bonds

The federal government doesn’t pay contractors the way private clients do. On a private job, a homeowner might pay in draws tied to progress. If the contractor disappears, the homeowner loses money and has to figure it out.

The government can’t operate that way on public projects. If a contractor walks off a school renovation or a corps of engineers building project, taxpayers are on the hook. Congress fixed this with the Miller Act.

The Miller Act (40 U.S.C. 3131) has been around since 1935. It requires that any prime contractor on a federal construction project over $150,000 must obtain a performance bond and a payment bond before the contract is signed. The contracting officer won’t execute the contract without them. If you win the bid and can’t produce the bonds, you lose the award.

The Three Types of Bonds

Bid bond. Required when you submit your bid, not after you win. It guarantees that if you’re selected, you’ll actually sign the contract and produce the required bonds. If you refuse after winning, the government can collect the difference between your bid and the next highest bid, up to the bond amount. Bid bonds are typically 20% of your bid total.

Performance bond. This guarantees you’ll complete the job according to the contract terms. If you default, the surety company either finds another contractor to finish the work or pays the government the cost to complete it. Performance bonds on federal work are typically 100% of the contract value.

Payment bond. This guarantees that all your subcontractors, suppliers, and laborers get paid. On private work, unpaid subs can file a lien against the property. On federal property, liens don’t work because the government owns the land. The payment bond is how subs and suppliers get protected on public jobs. Also typically 100% of the contract value.

When Bonding Is Required

The thresholds the Miller Act sets are:

Over $150,000: Both performance bond and payment bond required. 100% of contract value on each. No exceptions for prime contractors.

$35,000 to $150,000: The contracting officer has discretion. They can require a payment bond up to 100% of the contract value. Read the solicitation carefully. It will tell you what’s required in this range.

Under $35,000: No bonding typically required under federal law. Individual agencies may still ask for it. Check the solicitation.

Set-aside contracts under the SBA’s 8(a), HUBZone, or WOSB programs still follow the same thresholds. Being in a small business set-aside category doesn’t exempt you from the Miller Act.

What Bonding Actually Costs

Surety bonds aren’t insurance you pay into and never see again. They’re a credit product. The surety company is guaranteeing your performance to the government, and they charge a premium for taking on that risk.

Bond premiums on federal construction work typically run between 1% and 3% of the bond amount per year. At 1%, bonding a $500,000 contract costs you $5,000 upfront. At 3%, that same contract costs $15,000.

Where you fall in that range depends on your credit, your company financials, your experience record, and how busy you already are. A contractor with a few federal projects completed, clean financials, and good credit will get closer to 1%. A newer company with thin financials pays more.

Factor bond cost into every bid. It’s a real project expense, not a footnote.

How Sureties Evaluate You

A surety company is deciding whether to stake their money on your ability to finish the job. They look at four things:

Credit. Personal credit for small contractors, business credit if your company has a track record. Below 650 and most sureties will pass on you or require significant collateral.

Working capital. Sureties want to see that you have enough cash and liquid assets to fund the job before draws come in. They calculate your working capital ratio. If you’re financially stretched, the surety sees that as risk.

Experience. Have you completed projects of similar size and scope? A contractor who has built a $200,000 commercial renovation can probably be bonded for a $300,000 federal job. A contractor who has only done residential work under $100,000 asking for a $2 million bond is going to have a harder time.

Work in progress. Sureties track how much work you have under contract that isn’t yet complete. Too much open work relative to your capacity is a red flag. It means you might be overextended.

The SBA Surety Bond Guarantee Program

If you can’t qualify for bonding through a commercial surety on your own, the SBA has a program worth knowing about.

The SBA Surety Bond Guarantee Program is available to small businesses that have been denied bonding through the regular market. Under the program, the SBA guarantees up to 90% of the surety’s potential loss. That guarantee makes the surety more willing to issue bonds to contractors who don’t yet have the financial track record to qualify on their own.

The program covers federal contracts up to $9 million, or up to $14 million for certain defense contracts. It doesn’t make bonding free. You still pay a premium and the SBA charges a small fee. But it opens the door when the commercial market won’t.

To apply, you go through an SBA-approved surety agent, not directly to the SBA. The agent submits your application and the SBA reviews it. It takes longer than conventional bonding, so if you’re using this program, start the process well before a solicitation closes.

Find approved sureties at sba.gov.

How to Get Bonded

Start with a surety agent, not an insurance agent. Most insurance agents don’t write surety bonds and will send you in circles. You want someone who specializes in construction surety.

What you’ll need to provide:

- Two to three years of business and personal tax returns

- Current financial statements (balance sheet, profit and loss)

- A list of completed projects with dollar values

- A list of current projects in progress

- Personal financial statement

- Any existing lines of credit

The surety agent will evaluate all of this and either issue you a bond capacity or tell you what you need to do to qualify. Bond capacity is the maximum single contract value and aggregate contract value they will bond you for. Knowing your capacity before you start bidding federal work saves you from chasing contracts you can’t execute.

If You Can’t Get Bonded Yet

Not being able to get bonded right now is a data point, not a permanent condition. Most of the time it means one of a few things: credit needs work, you need more completed project history, or your working capital is too thin.

The practical path forward is to start on federal contracts under $35,000 where bonding isn’t required. Use those to build a track record. Document everything. Get your financial statements in order. After two or three completed federal jobs, go back to a surety agent. Your picture looks a lot different with a few government contracts on the books than it did without any.

You can also look at subcontracting under a prime contractor who is already bonded. You do the work, the prime holds the bond liability. It doesn’t build your prime contractor history as fast, but it gets you into federal work and builds relationships.

What to Look for in a Solicitation

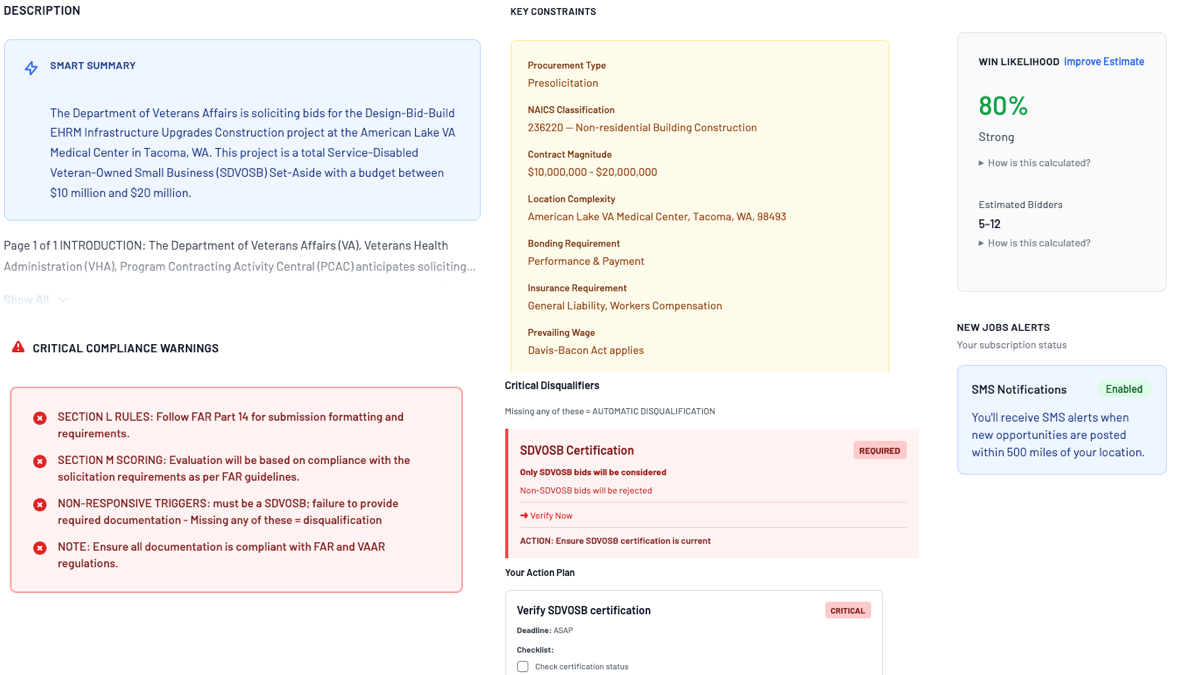

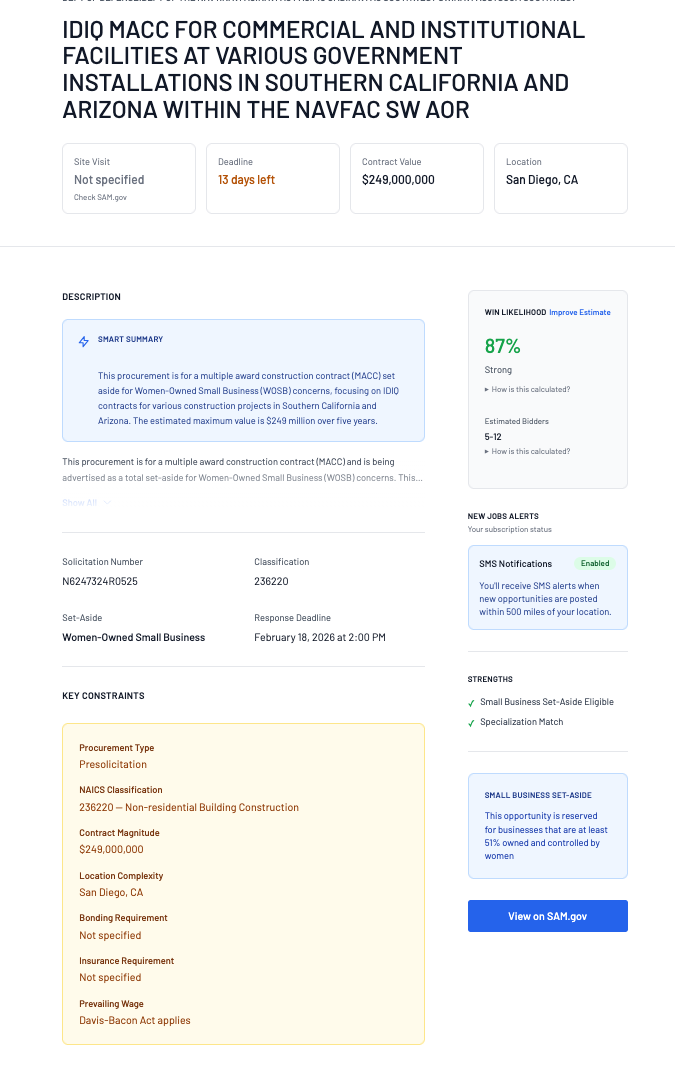

When you open a federal construction solicitation on SAM.gov, look for Section B or the attachments for bond language. The solicitation will state exactly what bonds are required, at what percentage of the contract value, and when they must be submitted. Some solicitations require the bonds at offer submission. Most require them within 10 days of award.

Don’t assume. Read it. Bond requirements vary by agency and sometimes by project type within the same agency.

If you’re using RenovationRoute to track federal opportunities, compliance flags for bonding requirements appear on each opportunity so you know before you spend time reading the full solicitation.

Bonding isn’t a bureaucratic obstacle. It’s a basic qualification for doing federal construction work. Get your bonding capacity established early, factor the cost into every bid, and treat the surety relationship like any other business relationship worth maintaining.